The history of the world is inextricably linked to the history of trade, in particular, the widespread trade of goods obtained on the back of atrocities and those capable of shaping our entire monetary system. In Tracking the Trade Winds, we look at the seismic importance of gold, sugar, silk, oil and more in connecting civilisations, enriching empires and facilitating the migration of people and resources.

In 1324, Mansa Musa, the emperor of the Mali Empire in West Africa embarked on a pilgrimage to Mecca, travelling across the Sahara Desert in a caravan accompanied by thousands of soldiers, servants, and merchants. Musa’s empire was blessed with an abundant reserve of gold.

![]()

As the caravan made its way through Egypt, Musa distributed gold generously, handing out coins to the poor, showering the cities he visited with gold dust, and funding the construction of mosques and educational institutions. His extravagant display of wealth had unintended consequences however, as the influx of gold devalued the currency and caused significant inflation in the regions he traversed.

It is also believed that his journey introduced West Africa, and its gold reserves, to the wider world, shattering preconceived notions and sparking interest in the region’s wealth. His pilgrimage serves as a powerful anecdote about the influence of gold and the impact it could have on global economies.

The gold standard was the basis of the international monetary system, under which the standard economic unit of account, such as the US dollar, was based on a predetermined amount of gold.

The gold standard was the basis of the international monetary system, under which the standard economic unit of account, such as the US dollar, was based on a predetermined amount of gold.

The discovery and spread of Gold

According to the National Mining Association, a US trade organisation, people most likely discovered gold in streams and rivers as early as 4000 BC. First believed to be used in Eastern Europe, for several thousands of years, it was primarily used to create jewellery and idols for worship.

Gold was first found in streams

Gold was first found in streams

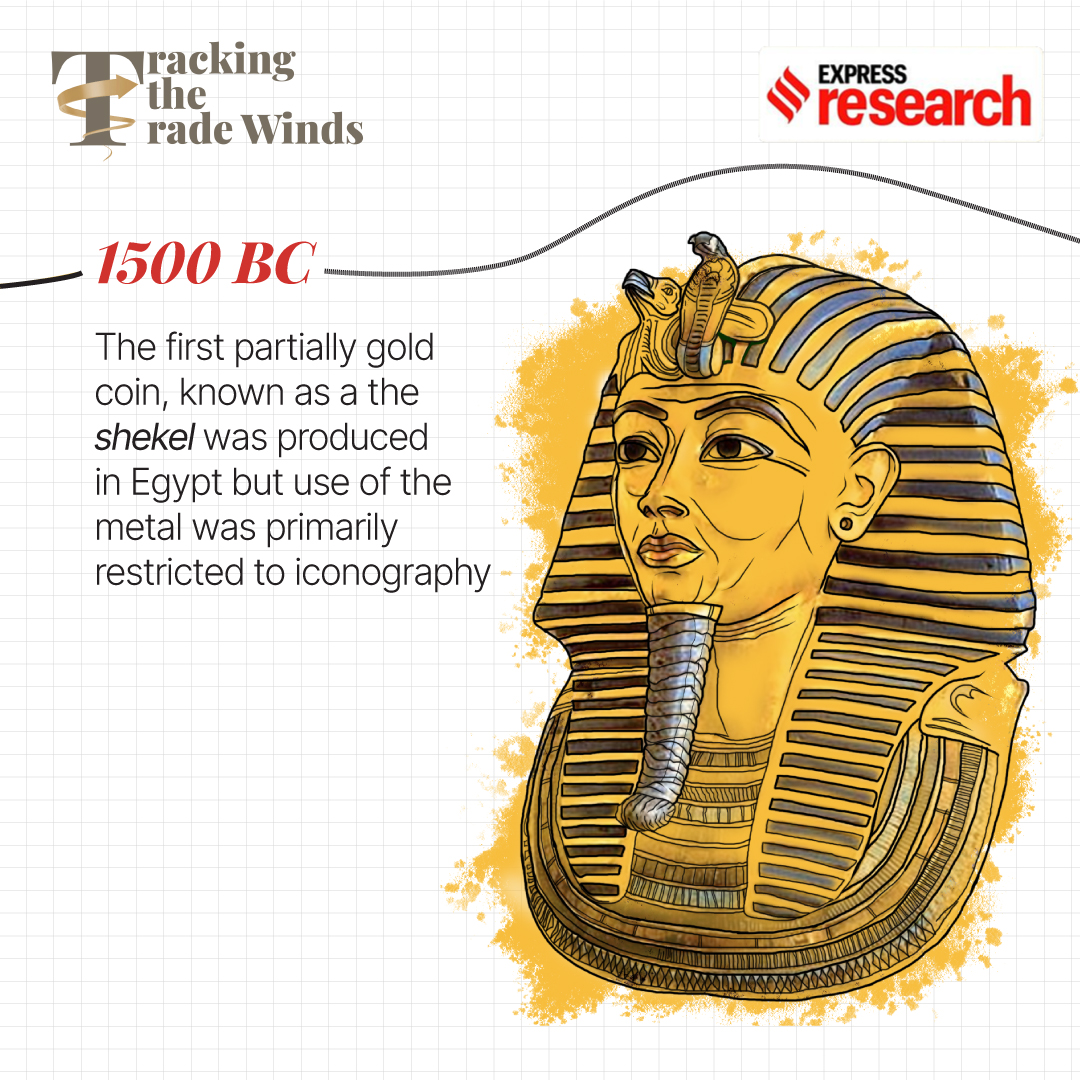

That changed in 1500 BC when the ancient empire of Egypt, containing the gold-rich region of Nubia, made the precious metal the first medium of exchange for international trade. Egypt created the shekel, a coin made from a naturally occurring alloy called electrum, which was around two-thirds gold and one-thirds silver.

Around the same time, the Babylonians discovered a method to test the purity of gold, a discovery that underpinned the commodity’s importance as an early barometer of economies. A few centuries later, in 1200 BC, the Egyptians discovered that they could mix gold with other metals in order to make it stronger and give it more variety in colour. Egyptians also began to experiment with a casting method known as lost-wax casting, in which a duplicate gold structure is cast from an original wax sculpture, allowing the alloy to be used in the design of intricate forms. As experienced seafarers, the Egyptians played a crucial role in disseminating gold across different regions.

In Egypt, gold was primarily used for ornamental purposes

In Egypt, gold was primarily used for ornamental purposes

Gold coins emerged a few centuries later in Lydia, a kingdom in Asia Minor, in 560 BC. In 50 BC, the Romans began the first minting of pure gold coins called Aureus. Till date, the symbol for gold in the periodic table, Au, comes from the Roman word for gold coinage. As the Romans maintained strong trade ties in Europe, Africa and Asia, gold coins used for trade and payments became a staple amongst those regions.

According to Roman author and philosopher Gaius Plinius Secundus, also called Pliny the Elder, the Romans were addicted to Indian luxury products and funded the purchase of the same with gold. In his book, Indian Feudalism, historian R S Sharma writes that Pliny derided this trade, believing that Indian exports were “unproductive luxuries” that were scarcely worth the gold that Rome was offering in exchange. However, despite Pliny’s concerns, gold was shipped extensively from Rome to Karachi Port (now in Pakistan), Gujarat and south India. As Charles Ernest Fayle writes in A Short History of the World’s Shipping Industry, “the beautifully built ships of the Yavanas came with gold and returned with pepper, and Muziris resounded with the noise.”

The Romans minted the first pure gold coin

The Romans minted the first pure gold coin

The scale of the trade is evident from the discovery of vast amounts of Roman gold coins and other artefacts from several sites in India including Pattanam in Kerala, Kolhapur in Maharashtra, and Coimbatore in Tamil Nadu. The British historian Peter Frankopan in his book The Silk Roads (2015) cites a Tamil poem that records the excitement over the Roman traders with gold: “The beautiful large ships…come bringing gold, splashing the white foam on the waters of the Periyar (river), and then return laden with pepper.” The abundant gold coins recovered from these sites in India have led historians to argue that local rulers in these regions, in all probability, made use of Roman gold and silver coins for their own currency or melted them for reuse.

Vast majorities of gold were shipped from Rome to India in exchange for spices

Vast majorities of gold were shipped from Rome to India in exchange for spices

Gold, because of its association with divinity, was especially revered in ancient India, with texts dating back as far as the Ramayana, describing the importance of gold in courts, palaces and religious institutions.However, despite India’s enduring fascination with the metal, the Indian subcontinent had few gold mines to speak of. The first small scale gold mine in India was said to have been Kolar in Karnataka around the 1st century. In 1880, the British engineering company John Taylor and Sons bought the Kolar Gold Fields and established India’s first industrial gold mine.

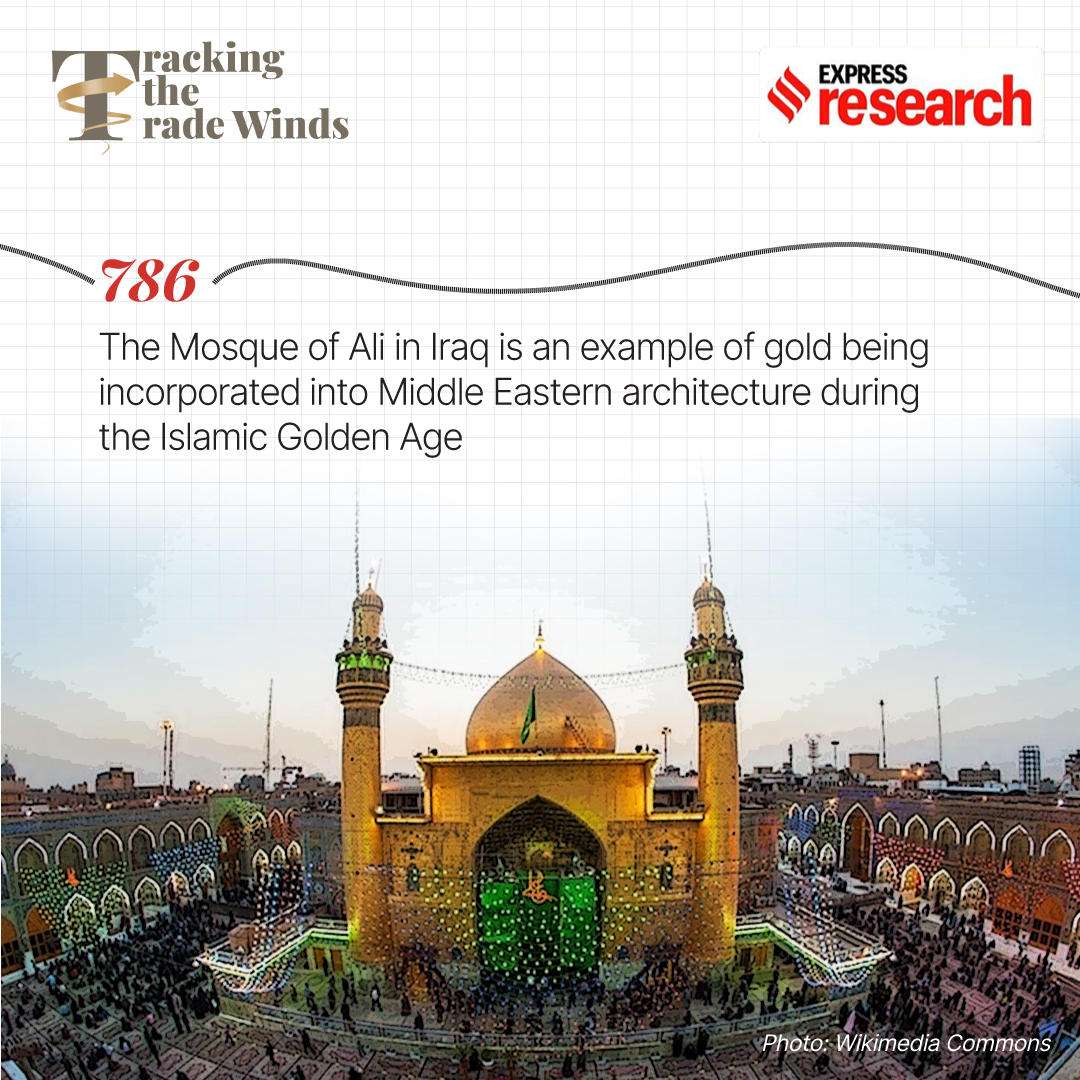

Gold was prominently featured in Middle Eastern architecture

Gold was prominently featured in Middle Eastern architecture

Like in India, gold also became especially popular in the Middle East during the Islamic Golden Age spanning from the 8th-14th century CE. The Islamic world was situated at the crossroads of major trade routes and during this time gold, along with other valuable commodities such as spices, textiles and precious stones, was traded extensively across these routes. Gold was also widely used as a medium of exchange and consequently, the Islamic gold dinar and silver dirham became widely recognised currencies within the Islamic countries. Gold also featured prominently in the architectural design of the Middle East, being used to decorate grand palaces and religious buildings.

During the age of exploration in the 15th and 16th centuries, European powers plundered vast quantities of gold from the Aztec and Inca civilizations. So much treasure was being transported from the New World to Europe during this time that the Spanish King Charles V was told in 1551 that “this period should more rightly be known as an era dorada – a Golden Age.”

However, possibly the biggest development in the history of this precious commodity was the discovery of Gold in California in 1848. As the prominent British economist E. Victor Morgan noted, the great increase in gold output following the discovery of the mines of California and Australia is “the most important single factor in the monetary history of the nineteenth century”.

Gold and the migration rush to the United States

The discovery of gold at Sutter’s Mill in California precipitated the largest migration in US history, bringing together people from the East Coast and around a dozen other countries, mainly China. Initially, almost all the immigrants were Chinese as Americans, lacking telegraph lines and railways, had to travel almost eight months from the West to East Coast to convey news of the discovery. In contrast, the journey from China by sea took only three months. It is estimated that in 1948, 20,000 Chinese immigrated to California, accounting for nearly 10 per cent of the state’s population during the 1850s. Immigrants also arrived from the Americas and Europe, leading author Mark Twain to remark that during that time, California had “the only population of the kind the world has ever seen gathered together.”

The California gold rush precipitated the largest migration in US history

The California gold rush precipitated the largest migration in US history

By 1849, news of discovery had spread to the East Coast, triggering an exodus to California. One way of measuring the impact of this discovery is in terms of population. In 1850, the US Census Bureau made its first count of the state, finding it to have 92,597 residents. By 1860, that number had quadrupled. However, not everyone who made the journey to California found good fortune. Many died en route, some faced inhospitable conditions and the prospect of back-breaking work, and others simply failed to find any gold on the land they staked. Those who were successful though, reaped the significant benefits of the Gold Rush, mining USD 81 million worth of gold in 1852. As Nathan Lewis points out in his book, Gold: The Final Standard, as a result of the discoveries in California, the international market for gold was transformed. He writes that global gold production “reached a peak of 227 tons in 1855, over thirteen times that 1830 level.”

The impact of the California gold rush spread rapidly across the globe. As the American academic James T. Phinney wrote in Gold Production and the Price Level, the Gold rush caused prices of gold to increase around the world, but in no country had its impact felt as deeply as that in the US. No longer did the nation have to depend mainly on capital brought by immigrants, or produced by imports. Instead, the coinage of gold increased the amount of money in circulation and produced a favourable trade balance for the United States.

However, the credit for making gold a truly global currency lies with the British.

The gold standard

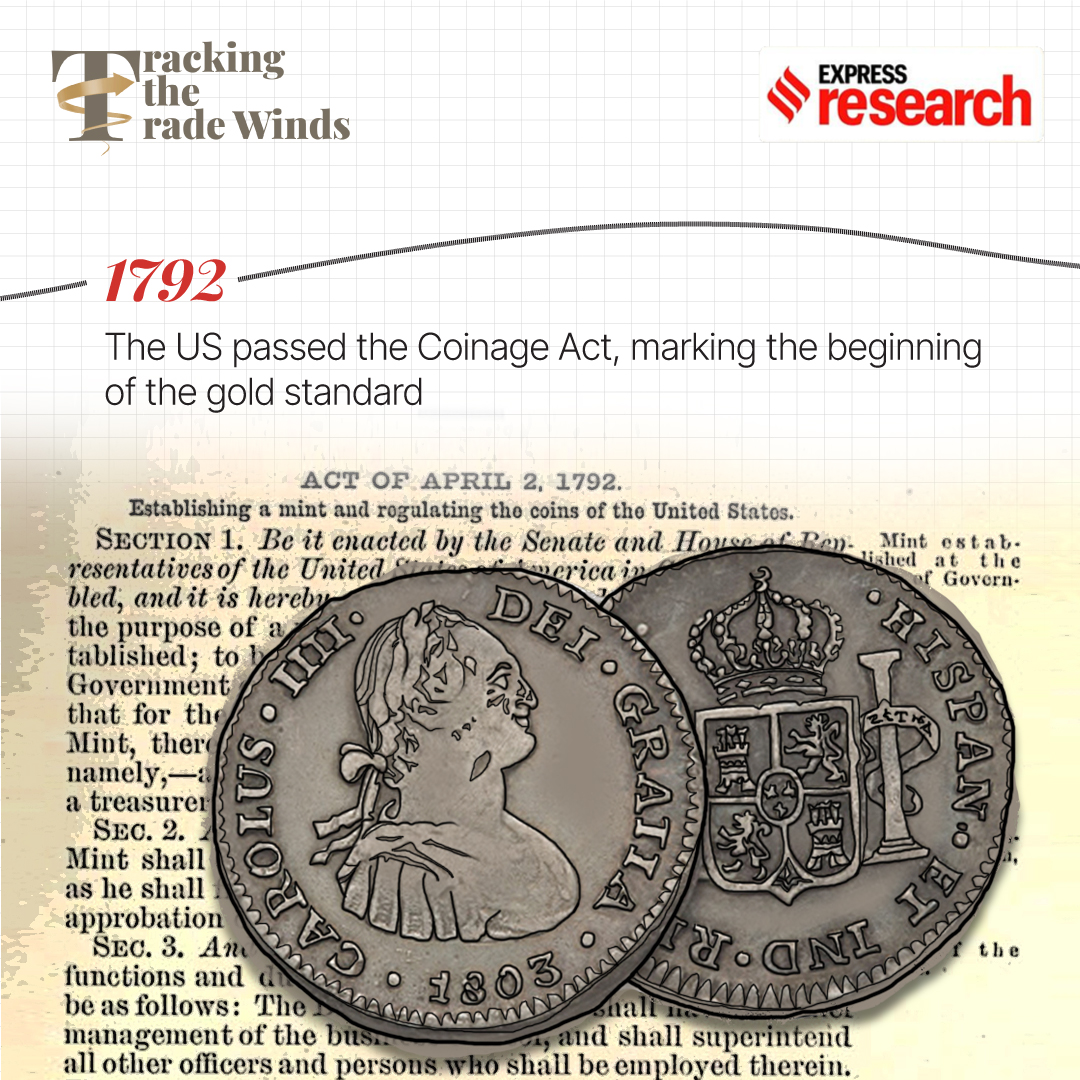

Ephraim Brasher, a goldsmith, produced the first gold coin of the United States in 1787. A few years later, in 1792, the fledgling American government passed the Coinage Act, putting the nation on a bi-metallic silver-gold standard that lasted until 1976.

The gold standard was the basis of the international monetary system, under which the standard economic unit of account, such as the US dollar, was based on a predetermined amount of gold. An individual with some paper money may visit a bank and exchange it for a certain amount of gold under this monetary system.

With the passage of the Coinage Act, the US formally adopted the gold standard

With the passage of the Coinage Act, the US formally adopted the gold standard

According to famed economist John Maynard Keynes, the history of our current monetary system began in the 19th century with the introduction of the gold standard. In his book, Indian Currency and Finance, he writes, “gold was the sole standard of value; it circulated freely from hand to hand; and it was freely available for export.”

The decline of the gold standard began in the early 20th century, fuelled by events such as the first World War and the Great Depression. Under the gold standard, the supply of money was directly linked to the supply of gold, which meant that if countries wanted to adjust inflation rates or increase money supply, they could only do it against their reserves of gold. This became a particular problem during the first World War when many nations decided to suspend the gold standard so that they could print money to pay for their military involvement in the war. This unrestricted printing of money caused hyperinflation, and after the war ended, countries began to appreciate the stabilisation that the gold standard had provided for their currencies and international trade.

The gold standard proved to inflexible for a globalised world and was eventually phased out

The gold standard proved to inflexible for a globalised world and was eventually phased out

However, the straw that broke the camel’s back was the Great Depression. After the stock market crash of 1929, European countries’ currencies were dangerously misaligned, especially with countries like Germany still recovering from the war. As people began to lose confidence in banks, gold hoarding became common, resulting in the spike of gold prices. As people started to rush the banks, the institutions rapidly began collapsing under the strain of significant withdrawals.

Soon, countries began to abandon the gold standard.

Today, no major country operates on a strict gold standard. The modern monetary system primarily relies on fiat currencies, which derive their value from the trust and confidence of users rather than a tangible commodity. However, gold still retains a vital role in the global financial system as a reserve asset and a store of value, attracting investors seeking stability and a hedge against economic uncertainties.

Most Read 1Chandrayaan-3 mission: Dawn breaks on Moon, all eyes on lander, rover to wake up 2As Indo-Canadian relations sour, anxiety grips Indian students, residents who wish to settle in Canada 3Karan Johar says Sanjay Leela Bhansali did not call him after Rocky Aur Rani: ‘He’s never called me but…’ 4Gadar 2 box office collection day 40: Hit by Shah Rukh Khan’s Jawan onslaught, Sunny Deol movie ends BO run with Rs 45 lakh earning 5Shubh’s tour in India cancelled: Why is the Canada-based singer facing the music?

Modern uses of gold

Although the gold standard is no longer in use, the metal remains an important commodity, being used in a variety of different sectors. Currently, the biggest producer and consumer of gold is China. India, despite not producing significant quantities of gold, is the second largest consumer of the metal. Although the price of gold has been volatile, dropping drastically in the early 2000s, it is currently priced at USD 1900 per ounce, compared to USD 300 in 1970 (adjusted for inflation at 2020 rates.)

According to the World Gold Council, 50 per cent of gold produced in the world is used for jewellery, 40 per cent for investments, and 10 per cent in industry. The value of gold in the jewellery and investment sectors is well established but lesser known is its importance in electronics. As gold is a corrosion free metal, it is used extensively in the production of cell phones, with each cell phone containing around 50 mg of gold according to the World Gold Council. Given that nearly one billion cell phones are produced per year, at 2022 prices, gold in cell phones represents a USD 2.82 billion market. Gold is also used in the production of semiconductor chips, televisions and aerospace exploration tools.

Also ReadThe many arguments for, and against, abortion rights How Lord Ganesha is celebrated outside IndiaKashmir when India got independence: Neither here nor thereHow Thakurs have dominated UP politics since Independence

Gold has played an integral role in shaping world history and continues to be an important commodity today. As Fernand Braudel, a French historian, remarked in 1946, “the chapters of world history…follow the rhythms imposed by the legendary metals.”